TSA Exponential Average (Array) VI

- Updated2024-07-30

- 3 minute(s) read

Performs exponential average on a univariate or multivariate (vector) time series. This VI returns a smoothed time series. Wire data to the Xt input to determine the polymorphic instance to use or manually select the instance.

Inputs/Outputs

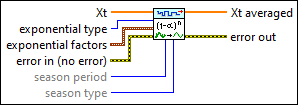

Xt

—

Xt

—

Xt specifies the univariate time series.  exponential type

—

exponential type

—

exponential type specifies the type of exponential average. Options include Single, Double, and Triple. The default is Single.  exponential factors

—

exponential factors

—

exponential factors specifies the weighting factors for exponential smoothing.

error in (no error)

—

error in (no error)

—

error in describes error conditions that occur before this node runs. This input provides standard error in functionality.  season period

—

season period

—

season period specifies the length of the seasonal pattern in the input time series. The default is 1. This option is available only when exponential type is Triple.

season type

—

season type specifies the way in which this VI models the seasonality. This option is available only when exponential type is Triple.  Xt averaged

—

Xt averaged

—

Xt averaged returns the averaged univariate time series.  error out

—

error out

—

error out contains error information. This output provides standard error out functionality. |

level

—

level

—

TSA Exponential Average Details

This VI uses the exponential weighting scheme to produce a smoothed time series. This VI computes the averaged values by assigning exponentially decreasing weights to the old values in the original time series according to the following equation:

Xa(i) = aXt(i-1) + a(1-a)Xt(i-2) + a(1-a)²Xt(i-3) +…

where a is the level weight for level cumulant Xa, Xa is the averaged time series, and Xt is the original time series.

Examples

Refer to the Exponential Smoothing VI in the labview\examples\Time Series Analysis\TSAGettingStarted directory for an example of using the TSA Exponential Average VI.